August 2, 2018 Lesjak Planning Perspective – Mid Year Comment

August 2, 2018 Lesjak Planning Perspective – Mid Year Comment

August 2, 2018 by Lesjak Planning

As we pass the midpoint of 2018, cross currents are evident in every market sector as well as worldwide which continues to keep investors on the sidelines. Even professional money managers have cash holdings in excess of the 10 year average. It seems as if the overwhelming consensus is that the equity markets are bound to have a major decline. Cash is being hoarded at next to nothing returns waiting to swoop in and buy shares more cheaply after the supposed decline.

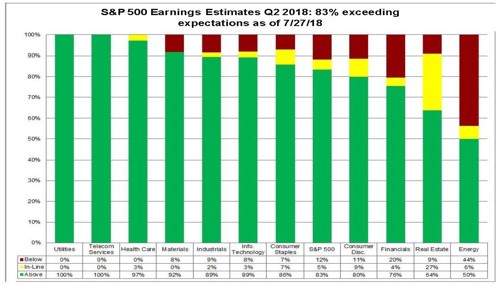

To date, even after the markets declined from their peak in late January, the S & P 500 is up 5.7%, Nasdaq plus 14%, and the Russell 2000 smaller company index is up 9.5%. On the plus side, so far during this corporate earnings season, 83% of the S & P 500 companies reporting have beaten their expectations. Our economy is growing at a better than average pace with reports of second quarter Gross Domestic Product coming in at over 4% growth. Unemployment rates across all categories of workers is at record lows. There are currently more job openings than individuals looking for work.

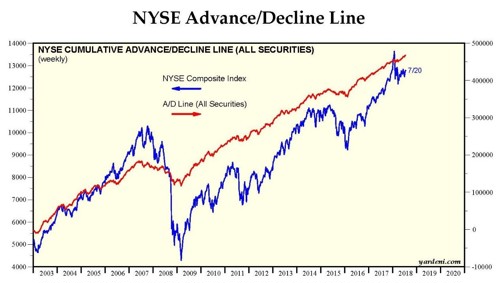

Although historical patterns are very useful in determining asset allocation, we have to look at current indicators to help with the most probable near term moves. Examples include the current state of the economy and corporate earnings. We touch on the fact that both are exceeding expectations currently. The tax law signed this year lowers corporate tax for many which increases profits and allows money kept overseas to be brought back to the States to be used for capital improvements and stock buybacks. Major market indices have also managed to stay above their 50 and 200 day moving averages (DMA) which confirms being in an uptrend. And one of the more effective tools used to determine how many stocks are actively participating in an uptrend is the Advance-Decline Line which is currently rising. Although there are no guarantees, these indexes and Advance-Decline Line should continue to point the way higher.

Mentioned earlier was the record amount of debt both personal and corporate borrowers have amassed. For the past ten years money has been cheap to borrow due to lifetime low interest rates. Corporations took advantage by issuing debt (bonds) at low rates and using the proceeds to buy back their stock, pay dividends to shareholders, or make capital improvements. While debt is generally not bad and is needed by most business’ at one time or another, there are a large number of companies that have large liabilities coming due to their bondholders over the next few years. If they borrowed too much in relation to their earnings and they cannot refinance when the bond matures, they will be in risk of default and bankruptcy. This is a major issue that will have to be watched.

On the personal debt side the picture is no better. Over the past 10 years, student debt has grown to a staggering $1.5 trillion. U.S. consumers owe more than $1 trillion on their credit cards and more than $1 trillion for auto loans. Households are drowning in debt and almost 73% of Americans now die in debt. The decision to keep interest rates so low for so long has encouraged the overuse of credit to buy now and pay (maybe?) later. As interest rates rise, it will only make the debt harder to pay back. We can only imagine that default rates will continue to increase and those holding the notes may regret their lax lending policies.

It is quite normal for there to be many factors that can either positively or negatively affect our economy and investment markets. This constant tug-of-war can cause emotional decisions with a short-term mindset – especially when exacerbated by our media. What gets lost though is the undercurrent of innovation, progress, and desire to succeed which are the foundation for future growth of our businesses. Those individuals with a prudent financial plan and long-term, patient approach to investing will benefit the most.

On the negative side for the market there are a number of fronts.

Getting the most headlines currently is the global trade and tariff negotiations. While each side’s chest thumping and threats may be no more than political posturing, the actions are causing substantial market volatility as buyers and sellers position for the possible outcomes of such actions.

Hopefully deals will eventually be struck which will not do harm to our domestic businesses that are affected by these threats to their international trade.

The Federal Reserve’s plan to get interest rates back up to the 3 – 3.5% area by 2020 can also hamper our economic growth if not careful. Any interest rate increase will greatly affect business’ ability to refinance the record amounts of debt that they have coming due between 2019 and 2021. If this debt cannot be refinanced, many companies that are over-leveraged will default and risk bankruptcy which will wipe out stockholders and bondholders alike. Toys R Us may be just one of many to disintegrate.

So, as we look at all of the positives and negatives that could affect our economy and investment markets, we look back and remember that history teaches that markets tend to do what hurts the most people the most. At this moment in time, with cash in such abundance on the sidelines waiting for a market decline, the most painful market direction would be up, trapping those on the sidelines again.

About the author

Lesjak Planning